As an international reinsurer, we see in many markets that only one of the two products is successfully established. In Asia, Disability insurance plays a very minor role compared to Critical Illness (CI) insurance in terms of premium volume. In Western Europe, on the other hand, the picture of premium volume is reversed. Disability insurance is widely sold there, while CI insurance is unknown to a large part of the population. In contrast, both products appear to be relatively well known in the Anglo-Saxon countries, although there are usually considerable differences in the premium volumes.

So, there seems to be a competition between the two insurance products. This may be since both products serve to close a financial gap caused by an accident or an illness. For example, both instruments can be used by insured persons to continue to pay a loan even though they are no longer able to generate income. As a result, after taking out CI or Disability insurance, the insured persons’ willingness to take out the other insurance product may decrease, as in their view another, apparently similar policy is not necessary.

Better protection by combining both products

The potential offered by a combination of the two insurance products for insureds seems to be untapped so far. The two products can be designed in such a way that they complement each other in a meaningful way and provide excellent cover for insured persons: disability insurance generally covers the loss of income due to accident or illness on a pro-rata basis, while CI insurance covers the financial requirements following an accident or an illness.

If insured persons have taken out Disability insurance, an additional CI insurance policy offers them the option of covering special costs. With the lump-sum payment made in the event of a claim, for example, insured persons could arrange for a particularly cost-intensive treatment that they have to pay for themselves or finance the conversion of their home if mobility is restricted in the long term due to the insured event.

Conversely, it may make sense to supplement existing CI insurance with Disability insurance. For example, the lump-sum payment can be used to cover special costs and the long-term financial consequences of an insured event can be cushioned with a pension benefit of a Disability insurance.

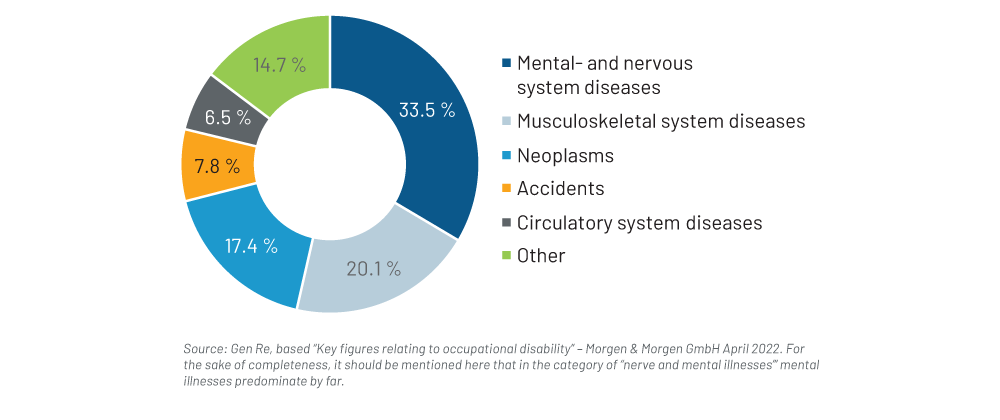

The different purposes of the types of cover are made clear by looking at the products’ benefit triggers. For example, musculoskeletal and mental illnesses are very rarely covered by CI insurance, although it has been proven that they can lead to financial distress for those affected. In the case of Disability insurance, however, these diseases now account for the lion’s share of claims, as illustrated by the example of German occupational disability insurance in the figure below. Cancer, myocardial infarction and stroke, which together typically account for 80%–90% of claims in CI insurance, rank only in third place (tumours) and in fifth place (heart and vascular diseases) among the causes of disability.

Causes of Occupational Disability