Economy

According to Stephen Cooper, Executive Director and Senior Economist for NCCI, the U.S. economy is in decent shape overall. Over 2023, real GDP grew by 3.1%. Against fears of a recession and the expected negative impact of interest rate hikes, the economy proved resilient. The first quarter of 2024 is off to a good start as well. As a result, along with favorable development regarding inflation data, consumer sentiment is starting to pick up. However, Mr. Cooper states there is always the potential for external shocks, such as global geopolitical events, which could negatively impact the economy. Thus far, it has remained resilient to recent events.

Labor Market

In 2023, three million new jobs were added to the labor market. Mr. Cooper states that 2024 is presently on track to add a similar amount. While the labor market is growing and the number of jobs currently exceed the amount that existed just prior to the pandemic, they still fall short of the pre-pandemic job growth trend-line. However, labor market churn has reduced significantly. The employee turnover rate and new hire rate have normalized to pre-pandemic levels. Low unemployment and solid hire rates point to a continuing strong labor market.

Regarding the overall U.S. population, the last of the baby boomer generation are nearing their retirement years. Population growth is slowing. By 2030, millennials and Generation Z will represent most of the labor force. As these two generation groups are smaller than those that came before it, the population continues to trend older.

Inflation / Interest Rates

According to Mr. Cooper, inflation slowed in 2023 after reaching a 40‑year high of 9%. Core CPI remains stubborn and includes core goods/services, housing and rents, and home and auto insurance. As of today, general inflation is at approximately 3.5% against the Feds target of 2% to 2.5%.

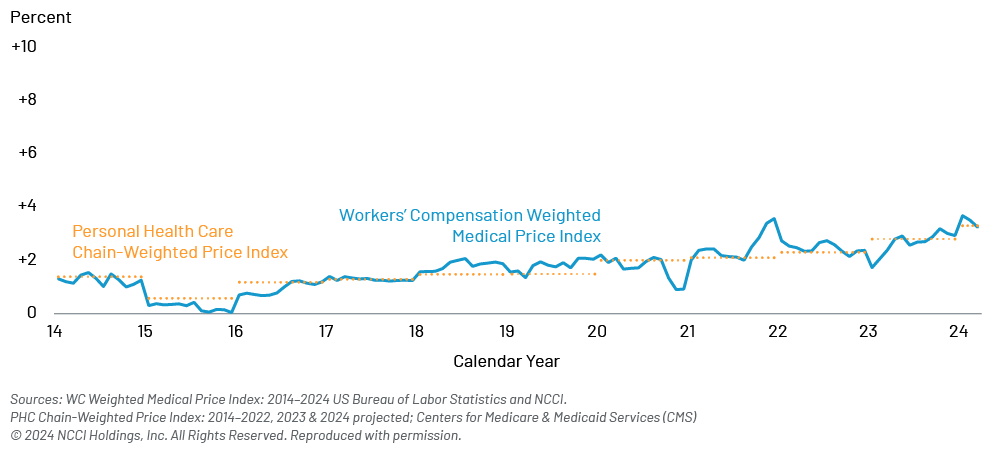

Medical inflation is separate from general inflation and its trend has been much more benign. While reviewing all medical indexes, NCCI also created the Workers’ Compensation Weighted Medical Price Index, which adjusts to specifically Workers’ Comp related medical costs. This index reflects medical inflation growing at a 2%‑3% trend, which is considered moderate. Medical costs that impact Workers’ Comp have both unique price trends and utilization trends for each type of medical service. Physician services has the highest distribution in terms of medical spend but traditionally sees the lowest level of price increases. The categories with the highest price pressure include hospital inpatient/outpatient care, but they represent an overall smaller share of total medical spend distribution.

Interest rates are higher, which has brought back investment income for the Workers’ Comp industry. While a gradual reduction is anticipated, possibly starting in 2024, the economy will dictate how quickly this may occur. It will depend on how both the labor market and inflation continue to evolve. The variability of these factors may result in interest rates remaining elevated for a longer period, which is a positive for investment income.

Workers’ Compensation Weighted Medical Price Index