Diet

In addition to limiting or ceasing use of tobacco, a healthy diet is an important aspect in managing one’s cardiovascular health risk. A diet full of fruits and vegetables, whole grains, nuts, fish, and poultry, together with reduced consumption of damaging foods such as red and processed meats and refined carbohydrates, could reduce one’s risk of heart disease by as much as 31%.8 Educating policyholders on the benefits of a healthy diet will go a long way in encouraging them to maintain a balanced diet.

Exercise

In August 2023, the world’s largest study9 published results showing that the more you walk, the lower your risk of death, even if you walk fewer than 5,000 steps per day. The analysis of 226,889 people from 17 different studies around the world has shown that the risk of dying from any cause or from cardiovascular disease decreases significantly with every 500 to 1000 extra steps you walk each day. An increase of 1000 steps a day was associated with a 15% reduction10 in the risk of dying from any cause, and an increase of as few as 500 steps a day was associated with a 7% reduction in dying from cardiovascular disease.

Financial Protection and Cardiovascular Disease – Are You Sufficiently Covered?

In addition to prevention, another important aspect to consider is protection against the financial burden for those who have suffered from CVD. These financial hardships could come from having to pay for the medical bills and from loss of income during treatment. This was the reason why Dr Marius Barnard, a cardiac surgeon who was a non-insurance practitioner, founded Dread Disease Insurance together with Crusader Life and with the support of Cologne Re (now Gen Re) in 1983.

Rapid scientific and technological advancement has tremendously increased the cost of managing CVDs. In addition, sustainability in healthcare financing across Asia have been under question in recent years with medical inflation being much higher than the general inflation. Therefore, at an individual level, having sufficient critical illness/medical insurance is the way to remove uncertainty from the burden of future healthcare costs.

Underinsurance and insurance protection gap is often a hidden threat. From Gen Re’s Dread Disease Survey, it has been observed that the median age at claim for CVD is in the early 50s, but the average issued age of policies are typically in the late 20s. The impact of inflation would be huge in this approximately 20 years gap between the point of policy issuance to point of claim.

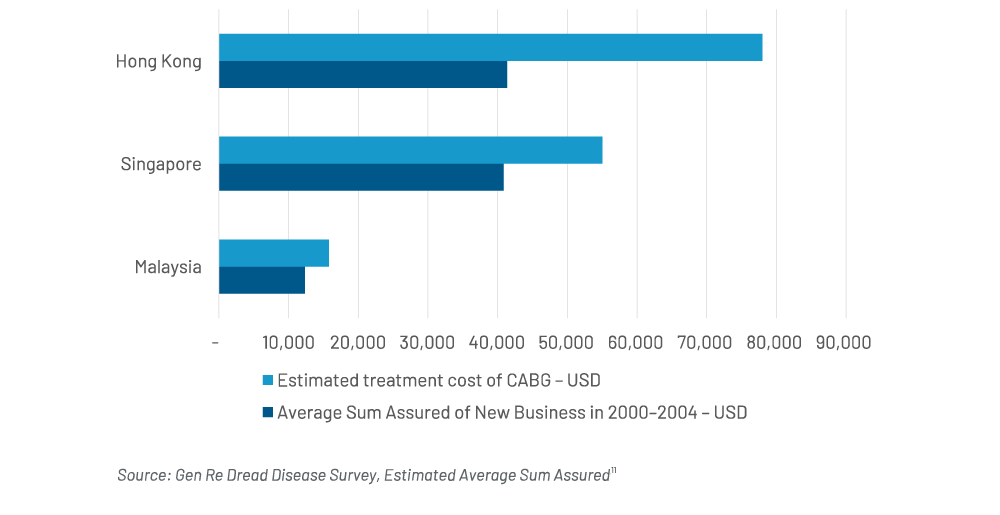

Following this logic, the figure below shows the estimated cost of a coronary artery bypass surgery in USD across different markets in a private hospital today, comparing it with the average sum assured of CI insurance issued approximately 20 years ago between 2000–2004. Clearly, the coverage provided by CI insurance purchased then is insufficient to pay for the medical treatment today.

Similarly, if we extrapolate this information, it is highly likely that the insurance coverage amounts bought today will also be insufficient to cover medical costs in the future. Therefore, with the rapid rise in medical inflation, one needs to re‑evaluate the adequacy of their Critical Illness insurance protection on a regular basis.

Comparison of Treatment Cost of CABG Today vs. Average Sum Assured When CI Was Originally Purchased (20 Years Back)